If you were rear-ended, it’s normal to start Googling things like:

“Average rear-end collision settlement”

“How much is my whiplash case worth?”

You want a number. Something concrete you can plan your life around.

Here’s the problem:

There is no single, reliable “average” settlement for a rear-end collision.

And any article that pretends there is is leaving out a lot of context.

This guide breaks down:

- Why “average settlement” numbers are often meaningless

- The main factors that drive value up or down

- Realistic ranges for different types of rear-end injury cases

- What you can do right now to protect the value of your claim

1. Why “Average Rear-End Settlement” Numbers Are So Misleading

When people throw around an “average” like $10,000 or $30,000 for a rear-end crash, they rarely tell you:

- Whether that includes tiny property-damage-only claims

- Whether it excludes very serious or fatal crashes

- The state, which massively affects value

- The policy limits involved

- How bad the injuries actually were

If you mix:

- A $1,500 minor soft-tissue claim,

- A $9,000 short-term whiplash case, and

- A $300,000 surgical case

…the “average” is a number that doesn’t look like any real case.

What matters much more than the “average” is where your case fits on the spectrum—from minor to catastrophic.

2. The Four Core Building Blocks of Settlement Value

Almost every rear-end collision settlement is built from some combination of these components:

1. Medical Bills (Past & Future)

- ER, urgent care, or hospital visits

- Primary doctor and specialist visits

- Physical therapy, chiropractic care, injections

- Imaging (X-rays, MRI, CT scans)

- Surgery and post-op rehab

- Prescriptions and medical devices (braces, TENS units, etc.)

General rule: the more necessary, well-documented treatment you have, the higher the potential settlement—up to policy limits.

2. Lost Wages and Loss of Earning Capacity

If your injuries force you to:

- Miss work completely

- Cut your hours

- Switch to a lower-paying job

- Quit a physically demanding career

…those lost earnings are part of your claim.

Short-term lost wages are based on pay stubs and employer letters.

Long-term or permanent losses may require expert opinion from doctors and vocational or economic experts.

3. Pain, Suffering, and Loss of Enjoyment

This is the non-economic side of your damages:

- Physical pain, headaches, muscle spasms

- Sleep problems

- Depression, anxiety, irritability

- Loss of ability to exercise, play with kids, travel, or enjoy hobbies

- Embarrassment or loss of independence

These are harder to put a number on, but they often make up a large part of serious cases—especially when there is surgery or permanent impairment.

4. Property Damage and Out-of-Pocket Costs

- Vehicle repair or total loss

- Towing and storage

- Rental car or rideshares

- Parking, mileage, and co-pays for medical visits

- Home help (cleaning, childcare) you had to pay for because of your injuries

Individually these may seem small, but together they add up and help show the real impact of the crash.

3. Key Factors That Push Your Settlement Up or Down

Two rear-end collisions with the same car damage can have totally different values. Here’s why.

A. Severity and Type of Injury

Rough spectrum (very general):

- Minor soft-tissue (short whiplash, a few PT sessions)

- Moderate soft-tissue (months of PT, possible injections)

- Disc injuries (herniations, nerve involvement)

- Fractures, concussions, or traumatic brain injuries (TBI)

- Surgical cases (neck/back fusions, shoulder surgery, etc.)

Each step up usually brings bigger bills, more time off work, and more suffering—which increases potential value.

B. Length and Consistency of Treatment

Insurers love to argue:

- “If you were really hurt, you wouldn’t have skipped appointments.”

- “You stopped treating for 2 months, so something else must have happened.”

Consistent, documented treatment:

- Shows you took your injuries seriously

- Makes it easier for doctors to connect your pain to the crash

- Leaves less room for the insurer to attack your case

C. Pre-Existing Conditions

Neck or back issues before the crash don’t automatically hurt your case. In fact, a collision can:

- Aggravate a pre-existing condition, or

- Turn a previously asymptomatic condition into a painful one

But insurers often use old records to argue that:

- “Your pain is from age, not the crash,” or

- “You would’ve had these problems anyway”

Good medical documentation can explain the difference between your before and after.

D. Liability (Who’s Actually at Fault)

Rear-end collisions are often straightforward—the rear driver is usually presumed at fault.

But things get more complicated if:

- You were brake-checking someone

- You reversed suddenly

- Your brake lights didn’t work

- There are multiple vehicles and chain-reaction impacts

If the insurer can pin part of the blame on you (comparative or contributory fault), it can reduce your settlement.

E. Policy Limits and Insurance Coverage

Sometimes your case is worth more than the available insurance.

Example:

- Your total damages reasonably support $150,000

- The at-fault driver only has $50,000 in liability coverage

- You don’t have enough underinsured motorist (UIM) coverage

In that situation, policy limits, not “case value,” may cap what you can recover from insurance.

F. Your State’s Laws

Your location can affect:

- How juries value pain and suffering

- Whether there are damage caps

- How comparative negligence works

- Deadlines to file suit (statutes of limitation)

That’s why local legal advice is so important.

4. Very General Settlement Ranges (With All the Caveats)

These are rough, educational ranges only—not predictions for your specific case.

- Minor soft-tissue rear-end collisions

- Few weeks–months of treatment, no missed work or just a few days

- Often low four figures to low five figures (for example: a few thousand to maybe tens of thousands, depending on bills and limits)

- Moderate soft-tissue or disc injuries without surgery

- Months of treatment, significant pain, some missed work

- Can move into mid–upper five figures or more, depending on documentation, impact on life, and policy limits

- Serious injuries with surgery, permanent restrictions, or major wage loss

- Long treatment, long recovery or permanent disability

- Can reach high five figures, six figures, or higher, especially with strong liability and higher insurance limits

Remember, these are broad educational ranges; many cases fall outside them because of policy limits, jurisdiction, or unique facts.

5. What Insurance Companies Look at When Valuing Your Rear-End Case

Insurers usually have internal software or guidelines. While they’ll never show you the formula, they tend to focus on:

- Total medical bills (and what they consider “reasonable”)

- Type and length of treatment

- Objective findings: MRI results, nerve tests, fractures

- Lost wages and employment history

- Any gaps in treatment

- Pre-existing conditions that might muddy the waters

- How credible you’d appear to a jury

Then they’ll weigh:

- How likely they are to lose at trial

- How much they might lose if a jury likes you more than them

The initial offer is often much lower than what they’re actually willing to pay—especially if you don’t have a lawyer.

6. Common Mistakes That Shrink Rear-End Collision Settlements

Avoid these if you can:

- Delaying medical care

Waiting days or weeks to see a doctor gives insurers an excuse to say the crash wasn’t that serious. - Skipping or stopping treatment too soon

Big gaps make them argue you were “fine.” - Not following medical advice

Ignoring recommendations for PT, imaging, or follow-up lets them claim you failed to “mitigate your damages.” - Oversharing with adjusters

Casual comments like “I’m feeling better” or “It’s no big deal” can appear later in cold, written form in your claim file. - Posting on social media

Photos of vacations, workouts, or nights out (even if you were in pain) can be twisted against you. - Settling before you know your long-term outlook

Once you sign a release, you usually cannot reopen the claim—even if you later need surgery.

7. How to Protect the Value of Your Rear-End Collision Claim

Here are practical steps that help your health and your case:

- Get checked out early.

Urgent care or your primary doctor is better than ignoring symptoms. - Be honest and detailed with doctors.

Explain all pain, even if it feels minor or embarrassing. If it’s not in the records, insurers will act like it doesn’t exist. - Stay consistent with treatment.

Follow through with PT, specialist visits, and recommended imaging as best you can. - Keep a simple pain and activity journal.

Note:- Pain levels (0–10)

- Tasks you struggle with (driving, sitting, lifting, playing with kids)

- Missed work and special events

- Save all receipts and correspondence.

Keep a folder (physical or digital) for:- Bills

- Letters/emails from insurers

- Photos of damage and injuries

- Consider consulting a personal injury attorney early.

Most offer free consultations and work on contingency (paid only if they recover money for you). A local lawyer can tell you:- How similar cases settle in your area

- Whether the insurer’s offer is in the right ballpark

- Whether it’s worth filing a lawsuit

8. FAQs About Rear-End Collision Settlement Amounts

“Can I calculate my settlement by multiplying my medical bills?”

Some people talk about 2x, 3x, or 5x of medical bills. Insurers used to rely more on that kind of formula. Today:

- In minor cases, they might offer something like a multiple of your bills.

- In serious cases, pain, suffering, and wage loss can be far more than a simple multiplier.

So: multipliers can be a rough starting point, not a reliable rule.

“Will a bigger car repair bill increase my injury settlement?”

Property damage isn’t everything, but:

- Heavy damage can support that the crash had serious force.

- Very light damage doesn’t automatically mean you aren’t hurt, but insurers will argue it.

Either way, focus on your medical records and symptoms, not just the body shop estimate.

“Do I have to accept the insurance company’s first offer?”

No. The first offer is often:

- Based on incomplete information, and/or

- A test to see if you’ll settle cheap and fast

You’re allowed to:

- Ask for a detailed breakdown of how they reached that number

- Submit more records or a counter-demand

- Talk to an attorney before you sign anything

“How long will it take to actually get paid?”

In many rear-end cases:

- Smaller, straightforward claims may settle in a few months.

- More serious or disputed cases can take many months or over a year.

- If your lawyer files a lawsuit, it may take 1–2+ years, depending on your court system.

A faster settlement is not always a better settlement.

Rear-end collisions are among the most common car accidents, often caused by distracted driving, tailgating, or sudden stops. While the at-fault driver (typically the one who rear-ends the other vehicle) is usually liable, settlement amounts can vary dramatically based on factors like injury severity, medical bills, lost wages, property damage, and state laws. There isn’t a single “average” payout—settlements are highly case-specific—but data from legal experts and case examples shows typical ranges from $2,000 for minor fender-benders to over $100,000 for serious injuries.

Key Factors Influencing Payouts

- Injury Severity: Minor soft-tissue damage (e.g., whiplash) leads to lower settlements; severe cases like spinal injuries or traumatic brain damage push amounts higher.

- Medical Expenses and Lost Wages: These form the economic core of claims, often multiplied by 1.5–5x for pain and suffering.

- Vehicle Damage: Repair costs or total loss value.

- Insurance Limits and Fault: Payouts are capped by policy limits; comparative negligence (e.g., if you’re partially at fault) reduces your share.

- Location: States like California or Georgia may see higher averages due to no-fault rules or denser traffic.

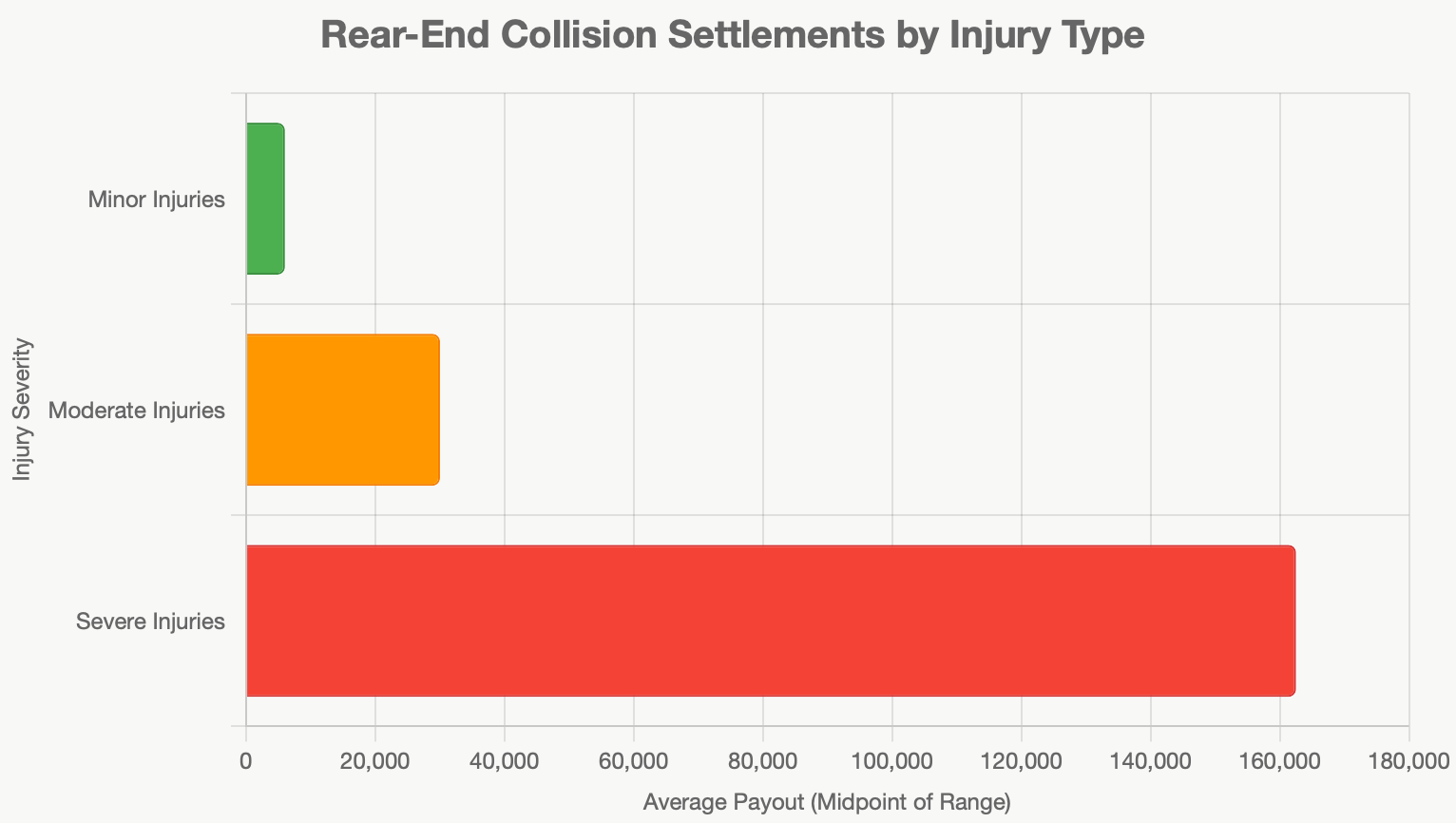

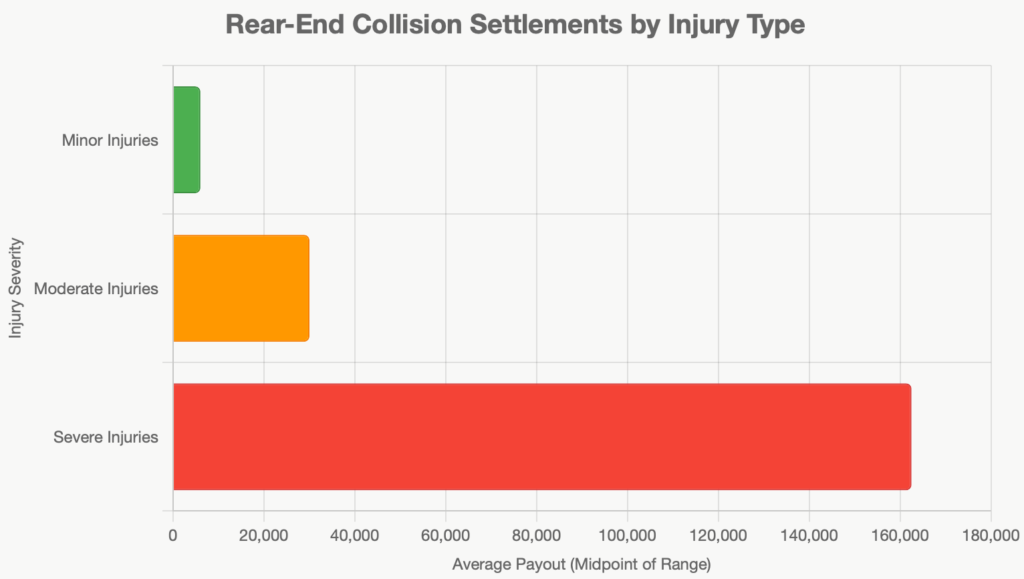

Typical Settlement Ranges by Injury Type

Based on aggregated data from personal injury law firms and case verdicts, here’s a breakdown of common payout ranges:

| Injury Severity | Description | Average Settlement Range | Examples |

|---|---|---|---|

| Minor | Soft-tissue injuries (e.g., whiplash, strains); low-speed crashes in parking lots or at stops. | $2,000 – $10,000 | Fender-bender with minor neck pain and quick recovery; covers basic medical visits and repairs. |

| Moderate | Herniated discs, back/neck injuries requiring therapy or short-term time off work. | $10,000 – $50,000 | Mid-speed collision with ongoing physical therapy; includes lost income and pain compensation. |

| Severe | Fractures, spinal damage, concussions, or long-term disability; high-speed or truck-involved crashes. | $75,000 – $250,000+ | Multi-vehicle pileup with surgery and permanent impairment; can exceed $1M in extreme cases. |

Overall U.S. average for injury-involved rear-end claims: $15,000–$30,000. For commercial truck rear-ends, expect $150,000–$200,000 due to higher damages.

Real Case Examples

- $300,000: Kansas driver rear-ended on icy ramp, leading to moderate injuries.

- $750,000: Missouri passenger in drunk-driver rear-end crash requiring neck fusion surgery.

- $1,075,000: Hit-and-run rear-end causing serious multi-body injuries.

- $30,000: Rear-ended by semi-truck with neck/back strain.

Visual: Settlement Ranges by Injury Severity

To illustrate the variation, here’s a bar chart showing average payout ranges across injury levels (based on the table above). The bars represent the low-to-high spectrum for each category.

Grok can make mistakes. Always check original sources.

Tips to Maximize Your Settlement

- Seek Immediate Medical Care: Document all injuries to build a strong claim.

- Gather Evidence: Photos, police reports, witness statements, and repair estimates.

- Avoid Early Settlement: Don’t accept the first insurance offer—consult a personal injury attorney.

- File Promptly: Statutes of limitations vary (1–4 years by state).

- Consider Legal Help: Attorneys often secure 3x higher payouts through negotiation or trial.

If you’ve been in a rear-end collision, your case’s value depends on specifics—use a free consultation with a lawyer for a personalized estimate. Always prioritize safety and recovery first.